Deductions

Get the scoop on your go-to deduction amounts and what interest you can write off.

Navigating taxes might not top your list of favorite activities, but having the right information at your fingertips? That’s a game-changer. This tax reference guide is your go-to resource for the most common rates, deductions, and credits—curated with small business owners in mind. We’ve done the heavy lifting so you can focus on what you do best: running your business.

Let’s make tax season less about stress and more about confidence.

Get the scoop on your go-to deduction amounts and what interest you can write off.

Compare IRAs, 401(k)s, and more to build a secure future—without drowning in fine print.

Easily check the latest per-mile rates and keep your records in tip-top shape.

Learn how to spread out asset costs (or write them off fast) to save on taxes over time.

Stay ahead of what you owe—whether you’re running payroll or flying solo.

Find out if this extra tax applies to your dividends, gains, or rental income.

Enjoy double benefits: save on healthcare costs and lower your tax bill all at once.

Discover how to claim a well-deserved break for supporting the next generation.

Understand the limits on tax-free giving, so you can share wealth without extra stress.

See exactly where your income fits into today’s brackets—no more guesswork.

| Filing Status | 2023 | 2024 | 2025 |

| Single | $13,850 | $14,600 | $15,000 |

| Head of household | $20,800 | $21,900 | $22,500 |

| Married filing jointly | $27,700 | $29,200 | $30,000 |

| Married filing separately | $13,850 | $14,600 | $15,000 |

| If blind or 65+, add * | |||

| Single | $1,850 | $1,950 | $2,000 |

| Head of household | $1,850 | $1,950 | $2,000 |

| Married filing jointly ** | $1,500 | $1,550 | $1,600 |

| Married filing separately | $1,500 | $1,550 | $1,600 |

You can deduct interest on your mortgage and home equity loans for your primary residence, but only if the funds were used to buy, build, or improve your home. The deduction limits depend on when the mortgage was taken out:

These limits apply for the 2022, 2023, and 2024 tax years.

| Description | 2023 | 2024 | 2025 |

| Contribution limits | |||

| If under 50 | $6,500 | $7,000 | $7,000 |

| If 50 or over | $7,500 | $8,000 | $8,000 |

| MAGI level when credit begins to phase out - covered by plan at work | |||

| Single | $73,000 | $77,000 | $79,000 |

| Head of Household | $73,000 | $77,000 | $79,000 |

| Married filing jointly | $116,000 | $123,000 | $126,000 |

| Married filing separately * | $ - | $ - | $ - |

| MAGI level when credit begins to phase out - not covered by plan at work | |||

| Single | N/A | N/A | N/A |

| Head of Household | N/A | N/A | N/A |

| Married filing jointly with a spouse who is not covered by a plan at work |

N/A | N/A | N/A |

| Married filing jointly with a spouse who is covered by a plan at work |

$218,000 | $230,000 | $236,000 |

| Married filing separately with a spouse who is not covered by a plan at work |

N/A | N/A | N/A |

| Married filing separately with a spouse who is covered by a plan at work * |

$ - | $ - | $ - |

A Traditional IRA is a classic choice for retirement savings—and for good reason. It allows you to contribute pre-tax dollars, which means you could lower your taxable income today while growing your savings tax-deferred until retirement. The best part? There’s no age limit for making contributions, so whether you’re 25 or 75, it’s never too late to invest in your future.

You also have some extra flexibility—contributions for the previous tax year can be made up until April 15th, giving you a little breathing room to maximize your retirement savings. Simple, straightforward, and effective, the Traditional IRA is a solid foundation for building your retirement nest egg.

A Roth IRA flips the script on retirement savings by letting you contribute after-tax dollars now, so your withdrawals (including earnings) in retirement are completely tax-free. It’s a smart option if you expect your tax rate to be higher in the future or simply like the idea of tax-free income when it counts the most.

Like the Traditional IRA, you can make contributions until April 15th for the previous tax year, and there’s no age limit—start saving at any stage of life. With its unique tax advantages, the Roth IRA is all about planting seeds today for a tax-free harvest tomorrow.

| Description | 2023 | 2024 | 2025 |

| Contribution limits | |||

| If under 50 | $6,500 | $7,000 | $7,000 |

| If 50 or over | $7,500 | $8,000 | $8,000 |

| MAGI level when credit begins to phase out | |||

| Single | $138,000 | $146,000 | $150,000 |

| Head of Household | $138,000 | $146,000 | $150,000 |

| Married filing jointly | $218,000 | $230,000 | $236,000 |

| Married filing separately * | $ - | $ - | $ - |

| Description | 2023 | 2024 | 2025 |

| Employee contribution limits | |||

| Employee (under 50) | $22,500 | $23,000 | $23,500 |

| Employee (50 or older) | $30,000 | $30,500 | $31,000 |

| Employer contribution limited to | |||

| This % of wages paid | 25% | 25% | 25% |

| or this $ amount | $66,000 | $69,000 | $70,000 |

| If you own your own business, that means you can effectively defer a total of |

|||

| If under 50 | $88,500 | $92,000 | $93,500 |

| If 50 or over | $96,000 | $99,500 | $101,000 |

A 401(k) is the workplace MVP of retirement plans, offering employees a chance to save for the future with pre-tax dollars while often enjoying the added bonus of employer matching contributions.

Here’s how the timeline works: Employee contributions must be made through W2 withholding by December 31st to count for the current tax year. Employers, on the other hand, have a bit more time—their contributions must be in by either the date the business files its tax return or the tax return due date (including extensions, if applicable).

A SEP-IRA (Simplified Employee Pension) is a great option for self-employed individuals and small business owners looking to provide retirement benefits for themselves and their employees. The standout feature? Only employers can contribute—employees aren’t allowed to chip in.

This plan is all about simplicity and flexibility for the employer, making it an efficient way to save for retirement without the complexity of other plans.

| Description | 2023 | 2024 | 2025 |

| Employee contribution limits | $ - | $ - | $ - |

| Employer contribution limited to | |||

| This % of wages paid | 25% | 25% | 25% |

| or this $ amount | $66,000 | $69,000 | $70,000 |

| Description | 2023 | 2024 | 2025 |

| Employee contribution limits | |||

| Employee (under 50) | $15,500 | $16,000 | $16,500 |

| Employee (50 or older) | $19,000 | $19,500 | $20,000 |

| Employer contribution limited to this percentage of wages paid | 3% | 3% | 3% |

A SIMPLE IRA (Savings Incentive Match Plan for Employees) is exactly what it sounds like: a straightforward way for small businesses to help employees save for retirement while keeping things manageable on the employer's end.

Employers have two options for contributing to the plan:

Keeping track of mileage for business, medical, or charitable purposes can help you maximize deductions and minimize guesswork. Use this table to quickly reference the IRS-approved mileage rates per mile for the current tax year:

| Description | 2023 | 2024 | 2025 |

| Business | $0.655 | $0.670 | $0.700 |

| Medical | $0.220 | $0.210 | $0.210 |

| Charitable | $0.140 | $0.140 | $0.140 |

Depreciation can feel like a maze of rules and percentages, but it’s an essential tool for maximizing your tax savings on business assets. This section simplifies the details, so you can confidently navigate the ins and outs of depreciating equipment, property, and other assets.

Depreciation rules set the foundation for claiming deductions on business assets. Not all assets are eligible—only those used for business purposes and with a useful life beyond a year qualify.

| Asset Life | Description |

| 3 Year (SL) | Most over the counter software |

| 3 Year (MACRS) | Dies, molds, small tools, certain livestock, tractor units |

| 5 Year (MACRS) | Certain vehicles, computers, office machinery, taxis, buses, trucks, cattle, private aircraft, appliances, carpeting, furniture & farm equipment |

| 7 Year (MACRS) | Certain manufacturing equipment, office furniture, printing equipment |

| 15 Year (MACRS) | Land improvements |

| 27.5 Year (MACRS) | Residential rentals, apartments |

| 39 Year (MACRS) | Nonresidential buildings |

Understanding depreciation rates is key to calculating your deductions accurately. This table provides the standard rates for common asset categories, assuming the mid-year convention (where assets are treated as placed in service at the midpoint of the year).

| Year | 3 year | 5 year | 7 year |

| Year 1 | 33% | 20% | 14% |

| Year 2 | 44% | 32% | 24% |

| Year 3 | 15% | 19% | 17% |

| Year 4 | 8% | 12% | 13% |

| Year 5 | - | 11% | 9% |

| Year 6 | - | 6% | 9% |

| Year 7 | - | - | 9% |

| Year 8 | - | - | 5% |

| Total | 100% | 100% | 100% |

Multiply the adjusted cost of your asset by the percentage shown in the table to determine your annual depreciation deduction. Note that percentages are rounded for simplicity, and longer-lived assets—like those with 15-, 27.5-, or 39-year recovery periods—are calculated using the straight-line method.

Bonus depreciation is a great way to maximize your deductions upfront, especially for assets with a recovery period of 15 years or less. This table outlines the applicable bonus rates, making it easy to determine the portion of an asset’s cost you can write off in the first year.

| Year | Rate |

| 2022 | 100% |

| 2023 | 80% |

| 2024 | 60% |

| 2025 | 40% |

| 2026 | 20% |

| 2027 | 0% |

Apply the bonus depreciation rate to the asset’s cost first. Once that’s calculated, apply the standard depreciation rates to the remaining balance to determine your total deduction.

Section 179 lets you deduct the full cost of qualifying assets in the year you buy them, but there are a few key limits. If your total purchases exceed the phaseout threshold, your maximum deduction is reduced dollar-for-dollar.

Also, Section 179 can’t create a taxable loss. If taking the full deduction would push your business into a loss, the extra amount rolls over to next year.

Use this table to quickly check the current limits and thresholds, so you can plan your deductions without any surprises.

| Description | 2023 | 2024 | 2025 |

| Maximum deduction | $1,160,000 | $1,220,000 | $1,250,000 |

| Phaseout starts at | $2,890,000 | $3,050,000 | $3,130,000 |

| Phaseout ends at | $4,050,000 | $4,270,000 | $4,380,000 |

When it comes to payroll and self-employment taxes, understanding the rates and thresholds is essential for staying compliant and maximizing your earnings.

One important note: If you earn more than $200,000, you may be subject to an additional Medicare tax of 0.9%. Be sure to account for this when calculating your total tax liability.

| Description | 2023 | 2024 | 2025 |

| Social security base | $160,200 | $168,600 | $176,100 |

| Social security rate | 12.40% | ||

| Medicare rate | 2.90% | ||

| Total for self employed | 15.30% | ||

| 1/2 for employee/employer | 7.65% | ||

| Description | Amount |

| Tax Rate | 3.80% |

| Applied when MAGI is above these amounts | |

| Single | $200,000 |

| Head of household | $200,000 |

| Married filing jointly | $250,000 |

| Married filing separately | $125,000 |

| Applied to the following types of income | |

| Interest | |

| Dividends | |

| Rental and royalty income | |

| Businesses that are passive activities | |

| Capital gains, including: | |

| Stock, bond and mutual fund sales | |

| Sale of investment real estate | |

| Sale of partnership or s-corp passive activities | |

The Net Investment Income Tax (NIIT) table is your cheat sheet for figuring out if this extra tax applies to you and what kind of income gets caught in its net. Here’s the deal: if your Modified Adjusted Gross Income (MAGI)—think of it as your AGI with a few tweaks—goes over certain thresholds, you could owe an additional 3.8% on certain types of income.

The table lays it all out for you:

Health Savings Accounts (HSAs) are a smart way to save for medical expenses while enjoying tax benefits. Whether you’re covered by an individual plan or a family plan, this table breaks down the contribution limits for each type of coverage.

A couple of things to keep in mind:

| Description | 2023 | 2024 | 2025 |

| Individual coverage | |||

| Deduction amount | $3,850 | $4,150 | $4,300 |

| Required minimum deductible | $1,500 | $1,600 | $1,650 |

| Family coverage | |||

| Deduction amount | $7,500 | $8,300 | $8,550 |

| Required minimum deductible | $3,000 | $3,200 | $3,300 |

| If 55+, add: | $1,000 | $1,000 | $1,000 |

| Description | 2023 | 2024 | 2025 |

| Amount per child | $2,000 | $2,000 | $2,000 |

| MAGI level when credit begins to phase out | |||

| Married filing jointly | $400,000 | $400,000 | $400,000 |

| All others | $200,000 | $200,000 | $200,000 |

The Child Tax Credit offers some much-needed financial relief to families, but there are a few details to keep in mind. This table outlines the credit amounts, income limits, and eligibility criteria so you can easily see where you stand.

Here’s the key part: If your Modified Adjusted Gross Income (MAGI) is above the listed thresholds, the credit starts to shrink. Specifically, for every $1,000 your income exceeds the threshold, the credit is reduced by $50.

Planning to share the wealth? The gift and estate tax exclusions help you pass on assets without triggering unnecessary taxes. This table breaks down the annual gift exclusion limit and the lifetime estate and gift tax exemption, making it easy to understand how much you can give or transfer tax-free.

| Description | 2023 | 2024 | 2025 |

| Gift tax exclusion | |||

| Single (one person) | $17,000 | $18,000 | $19,000 |

| Married (gift splitting) | $34,000 | $36,000 | $38,000 |

| Lifetime exclusion | |||

| Single (one person) | $12,920,000 | $13,610,000 | $13,990,000 |

| Married (gift splitting) | $25,840,000 | $27,220,000 | $27,980,000 |

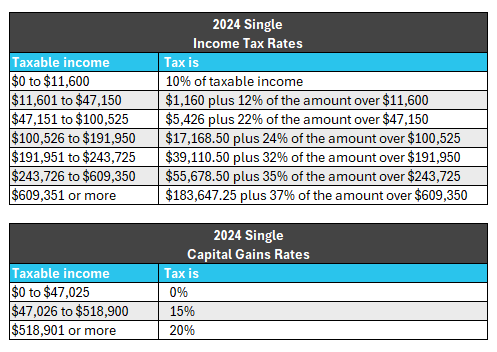

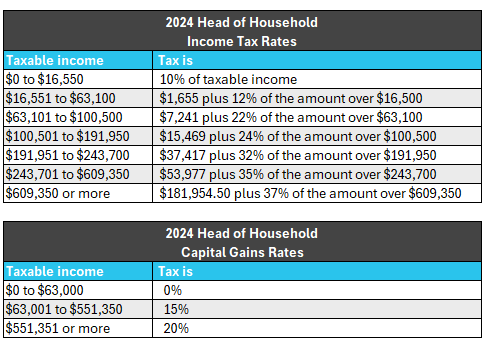

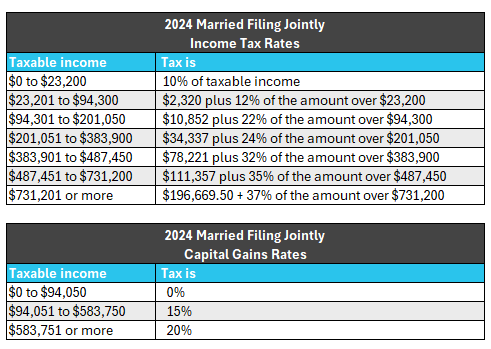

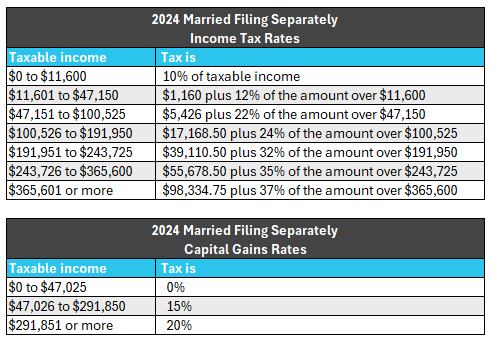

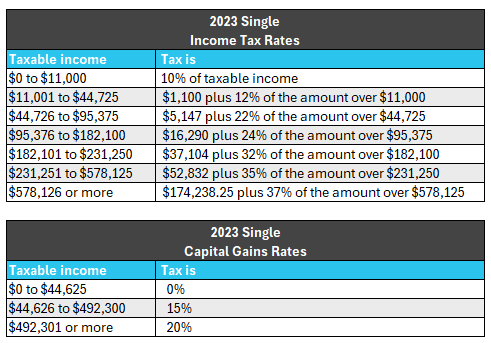

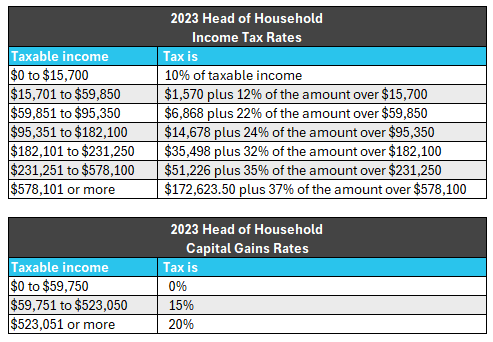

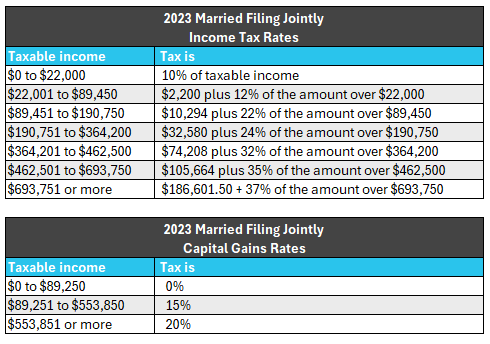

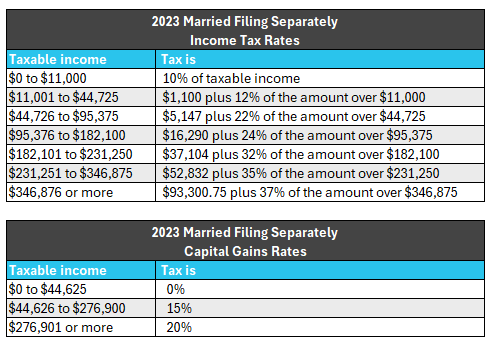

Filing jointly? Single? Head of household? We’ve got you covered.

Below you'll find the cheat sheet you didn’t know you needed for figuring out what slice of your earnings Uncle Sam is taking. Spoiler: It’s probably not as bad as you think. Or maybe it is—but at least you’ll know for sure!

| Taxable income | Tax is |

| $0 to $11,925 | 10% of taxable income |

| $11,926 to $48,475 | $1,192.50 plus 12% of the amount over $11,925 |

| $48,476 to $103,350 | $5,578.50 plus 22% of the amount over $48,475 |

| $103,351 to $197,300 | $17,651.00 plus 24% of the amount over $103,350 |

| $197,301 to $250,525 | $40,199.00 plus 32% of the amount over $197,300 |

| $250,526 to $626,350 | $57,231.00 plus 35% of the amount over $250,525 |

| $626,351 or more | $188,769.75 plus 37% of the amount over $626,350 |

| Taxable income | Tax is |

| $0 to $48,350 | 0% |

| $48,351 to $533,400 | 15% |

| $533,401 or more | 20% |

| Taxable income | Tax is |

| $0 to $17,000 | 10% of taxable income |

| $17,001 to $64,850 | $1,700 plus 12% of the amount over $17,000 |

| $64,851 to $103,350 | $7,442 plus 22% of the amount over $64,850 |

| $103,351 to $197,300 | $15,912 plus 24% of the amount over $103,350 |

| $197,301 to $250,500 | $38,460 plus 32% of the amount over $197,300 |

| $250,001 to $626,350 | $55,484 plus 35% of the amount over $250,500 |

| $626,351 or more | $187,031.50 plus 37% of the amount over $626,350 |

| Taxable income | Tax is |

| $0 to $64,750 | 0% |

| $64,751 to $566,700 | 15% |

| $566,701 or more | 20% |

| Taxable income | Tax is |

| $0 to $23,850 | 10% of taxable income |

| $23,851 to $96,950 | $2,385 plus 12% of the amount over $23,850 |

| $96,951 to $206,700 | $11,157 plus 22% of the amount over $96,950 |

| $206,701 to $394,600 | $35,302 plus 24% of the amount over $206,700 |

| $394,601 to $501,050 | $80,398 plus 32% of the amount over $394,600 |

| $501,051 to $751,600 | $114,462 plus 35% of the amount over $501,050 |

| $751,601 or more | $202,154.50 + 37% of the amount over $751,600 |

| Taxable income | Tax is |

| $0 to $96,700 | 0% |

| $96,701 to $600,050 | 15% |

| $600,051 or more | 20% |

| Taxable income | Tax is |

| $0 to $11,925 | 10% of taxable income |

| $11,926 to $48,475 | $1,192.50 plus 12% of the amount over $11,925 |

| $48,476 to $103,350 | $5,578.50 plus 22% of the amount over $48,475 |

| $103,351 to $197,300 | $17,651 plus 24% of the amount over $103,350 |

| $197,301 to $250,525 | $40,199 plus 32% of the amount over $197,300 |

| $250,526 to $375,800 | $57,231 plus 35% of the amount over $250,525 |

| $375,801 or more | $101,077.25 plus 37% of the amount over $375,800 |

| Taxable income | Tax is |

| $0 to $48,350 | 0% |

| $48,351 to $300,000 | 15% |

| $300,001 or more | 20% |

| Taxable income | Tax is |

| $0 to $3,150 | 10% of taxable income |

| $3,151 to $11,450 | $315 plus 24% of the amount over $3,150 |

| $11,451 to $15,650 | $2,307 plus 35% of the amount over $11,450 |

| $15,651 or more | $3,777 plus 37% of the amount over $15,650 |

| Taxable income | Tax is |

| $0 to $3,250 | 0% |

| $3,251 to $15,900 | 15% |

| $15,901 or more | 20% |

| Taxable income | Tax is |

| $0 or more | 21% flat rate |

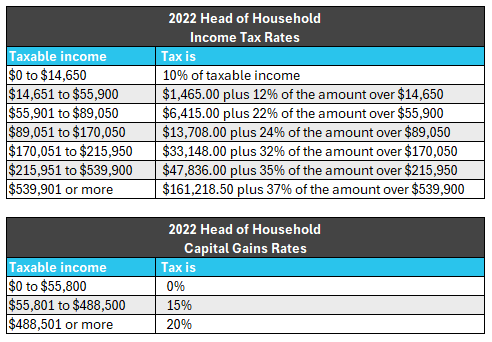

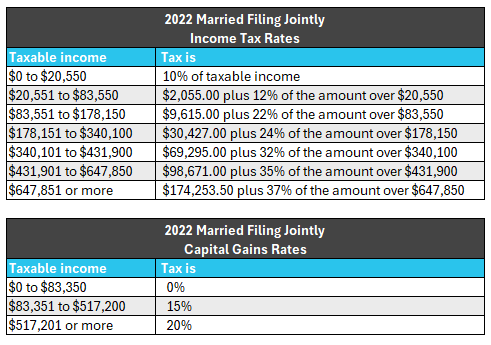

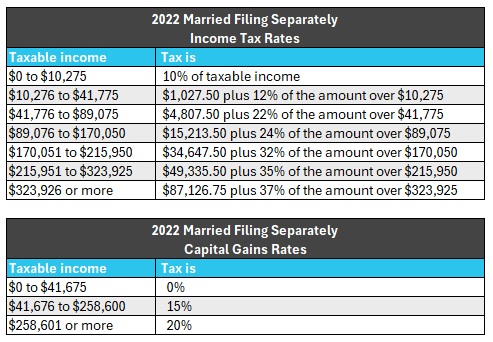

Feeling nostalgic for tax rates of years gone by? Probably not, but if you need them, we’ve got them. This section shows federal income tax rates for the last three years, so you can compare and see how the numbers stack up.

Looking to dive deeper? Our Learning Center is packed with articles designed to make even the trickiest tax topics feel manageable. From decoding deductions to mastering credits, we break it all down in plain English—no accounting jargon required. Here are just a few of those resources we think you might like.

You can pay your taxes online in a few quick and easy steps with Direct Pay.

The IRS estimates that business owners spend an average of 22 hours filing their tax return. Luckily, it only takes a few...

Keep track of the most important deadlines this year.

There's a lot you need to keep track of for your federal and/or state tax needs. We've listed the due dates for the most common IRS forms you...

The answer will probably not surprise you.

If you deal with significant amounts of cash on a regular basis, you might be wondering what, if anything, you are required to say to the IRS. The answer is...