Receiving a tax notice or letter is never a pleasant experience. It can be confusing and frustrating if you don't understand why you received the notice in the first place. That's why we wrote The Ultimate Guide to Tax Notices and created a tax notice library filled with the most common tax notices and letters you might receive. We believe the process of staying compliant with your taxes should be as effortless as possible.

General Information

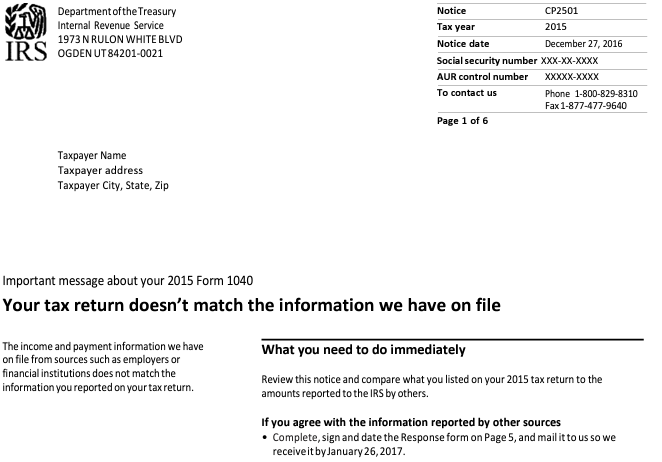

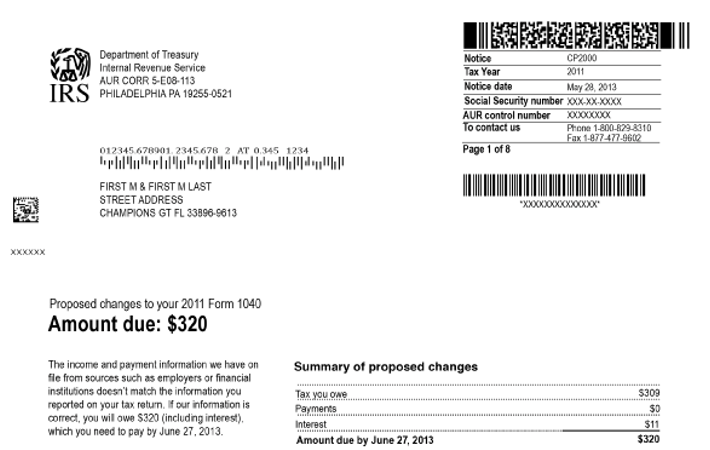

- What is the notice number? CP2000

- What government agency sends this notice? The Internal Revenue Service (IRS)

- What is this notice about? The income or payment information the IRS received from third parties, such as employers or financial institutions, doesn't match the information you reported on your tax return. This discrepancy may cause an increase or decrease in your tax or may not change it at all. The notice explains what information the IRS used to determine the proposed changes to your tax return.

- What should you do if you receive this notice?

- Read your notice carefully. It explains the information the IRS received and how it affects your tax return.

- Provide a timely response. If you need additional time to respond, you can request an extension by mailing or faxing in the request, or by calling the toll-free number shown on the notice.

- Complete the notice response form and state whether you agree or disagree with the notice. The response form explains what actions to take. (Your specific notice may not have a response form. In that case, the notice will have instructions on what to do). You can submit your response by:

- Mail using the return address on the enclosed envelope, or

- Fax your documents to the fax number in the notice using either a fax machine or an online fax service. Protect yourself when sending digital data by understanding the fax service’s privacy and security policies.

- If you agree with the proposed changes, follow the instructions to sign the response form. The IRS requires both spouses' signatures if you filed married filing jointly.

- If you disagree, complete and return the response form. Provide a signed statement explaining why you disagree and supply any documentation, such as a corrected W-2, 1099, or missing forms, to support your statement.

-

- If the information reported to the IRS is not correct, contact the business or person who reported the information. Ask them for a corrected document or a statement to support why it is in error, then send the IRS a copy with your response.

- Respond by the due date shown in the notice. If you don't respond, the IRS will send you a Statutory Notice of Deficiency followed by a bill for the proposed amount due.

FAQs & Additional Information

- Make sure your other returns don't have the same mistake. If they do, file Form 1040-X, Amended U.S. Individual Income Tax Return, to correct the mistakes.

- Contact the IRS with any unanswered questions you have or if you need time to respond to the notice. If you contact them by phone, keep in mind call volumes may be high and it could take some time to reach a representative.

- Review Publication 5181, Tax Return Reviews by Mail: CP2000, Letter 2030, CP2501, Letter 2531

- Keep a copy of the notice for your records.

- Complete section 3 (authorization) on the response form if you want to allow someone, in addition to yourself, to contact the IRS about this notice. Or, send them a Form 2848, Power of Attorney and Declaration of Representative to allow someone (such as your tax return preparer) to contact them on your behalf.

- Correct the copy of your tax return that you kept for your records.

- Order a transcript of your return, if needed.

- Learn more about your payment options if you owe additional taxes. Interest continues to accrue until the unpaid balance is paid in full and penalties may apply.

- Learn more about payment plans and installment agreements, if you cannot pay the full amount of taxes owed.

- Learn more about Offers in Compromise, if you cannot pay the full amount of taxes owed.

- Do I have to reply to this notice? No, contact the number listed on the notice. The SSA can't stop the levy or assist you in resolving the tax issue.

- How do I make my repayment?

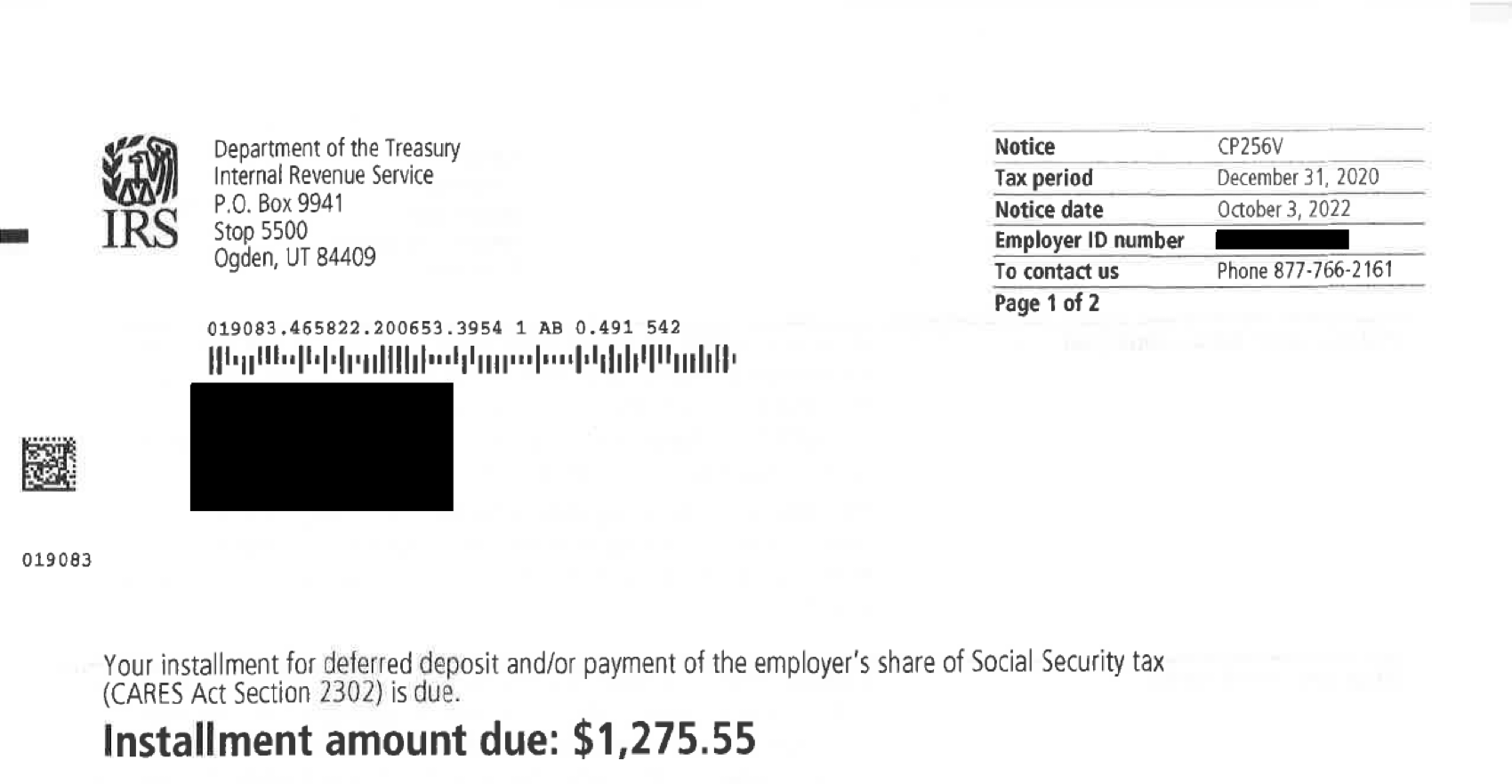

- You can make the deferral payments through the Electronic Federal Tax Payment System (EFTPS), by credit or debit card, or with a check or money order. Note: you must make these payments separate from other tax payments to ensure they're applied to the deferred payroll tax balance. IRS systems won't recognize the payment if it's with other tax payments or sent as a deposit.

- To make the deferred payment using EFTPS, select deferral payment and change the date to the applicable tax period for the payment. You can visit eftps.gov or call 800-555-4477 or 800-733-4829 for details.

- If the employee no longer works for the organization, you must repay the entire deferred amount of the employee's portion of Social Security tax then collect the employee's portion using your own recovery methods.

- How do I make a payment for a deferred amount on an aggregate return?

- Third-party payers (such as an Internal Revenue Code Section 3504 agent, a certified professional employer organization, a non-certified professional employer organization, or other agents designated with Form 2678, Employer/Payer Appointment of Agent) file aggregate returns to show the employer's deferred tax.

- Employers should coordinate with their third-party payer to pay deferred taxes owed by the December 31, 2021, and December 31, 2022, due dates. This helps ensure the third party properly records the payment and the correct employer identification number (EIN) and tax period are noted with the payment so the IRS can apply it properly.

- Employers should continue coordinating with their third-party payer to ensure payments are applied under the third party's EIN (unless the employer receives an IRS notification stating the unpaid deferral amount has been moved to their EIN).

- What if I cannot pay my deferred taxes? You may be eligible for a payment plan or other payment options. Note: if the IRS don't receive your payment by the applicable due dates, the deferred taxes may be subject to Failure to Deposit penalties.

- How do third-party payers report unpaid deferred amounts from aggregate returns? Employers are solely responsible for payment of the deferred taxes they requested for any wages paid by the third-party payer. If the third-party payer filed an aggregate return and receives a balance due notice for the employer's unpaid portion of deferred Social Security tax, the third-party may notify the IRS by eFax. Fax your information to 844-255-1856 using either a fax machine or an online fax service. Protect yourself when sending digital data by understanding the fax service’s privacy and security policies. Please include a cover sheet with the following information:

- Copy of the Schedule R (Form 941 or 943) for relevant tax periods

- Client (common law employer) name, EIN, and current address

- Total deferred amount per tax period

- Unpaid part of the deferred amount, per tax period

- List of deferral payments by client or by the third-party payer on behalf of client(dates and amounts), per tax period

- If applicable, date client separated from aggregate filer

What does it look like?

Resources

Looking for more information about this notice? Here are some helpful resources:

- About the notice - https://www.irs.gov/individuals/understanding-your-cp2000-notice

How can we help you today?

Are you looking for more information about your tax notice or other challenges? DiMercurio Advisors has a dedicated team supporting tax notices, audits and more. We are passionate about ensuring you are well-informed and in control of your tax situation.